The 60/40 is Dead …

Long Live Modern Portfolio Theory

The 60/40 portfolio, comprised of 60 percent equity benchmarks and 40 percent bonds, has remained a cornerstone of the wealth management industry for many decades. Its enduring value and efficiency as an optimal allocation strategy – i.e., the highest return for a certain level of risk – have solidified its status as a benchmark for moderate risk investment strategies that can be tailored and tweaked into variations, e.g., conservative (or 20/80), and aggressive (or 80/20) portfolio. Yet, the recent surprising and disappointing performance of the strategy has triggered a fierce debate over its long-term value. This debate however misses the forest for the tree. While the 60/40 cookie-cutter practice is indeed obsolete, the criticism over its validity has, if anything, renewed interest in efficient and optimal portfolio construction in line with Markowitz’s teachings and at the core of the 60/40 approach itself! Indeed, with today’s avalanche of free data, computing power, AI, digital platforms, financial innovation, and availability of low-cost ETFs and zero-commission brokers, there is tremendous scope to build highly diversified and customized portfolios closely matching the investor’s risk tolerance profile and goals … a quantum leap from the cookie-cutter 60/40 dull strategy and its indiscriminate conservative, moderate, and aggressive variations.

First, some history …

The 60/40 approach is possibly the most popular application of Markowitz’s Nobel Prize-studded Modern Portfolio Theory (MPT). Markowitz’s seminal work is founded on a fundamental mathematical observation: when the components of a portfolio are not perfectly correlated, the overall risk of the portfolio, measured by the standard deviation of returns, will be lower than the weighted sum of the risks of individual components. Additionally, if there exists a negative correlation (as advocated by economic theory) between assets such as bonds and equities, losses incurred in one asset class can be offset by gains in the other. In essence, Markowitz’s work emphasizes the power of diversification in portfolio management. By intelligently selecting assets with low correlation or negative correlation, investors can potentially achieve higher returns for a given level of risk or reduce risk for a desired level of return—a concept often described as the “free lunch” in finance.

In addition to the academic rigor, the 60/40 portfolio gained popularity due to its simplicity in execution. Typically, this strategy involves investing in two or three broad equity benchmarks, predominantly focused on the US market with some allocation to international equities and a smaller portion in emerging markets. Similarly, it entails allocating to a couple of bond benchmarks, primarily US-based with some international and corporate exposure for added diversification. John Bogle, renowned as the father of passive investment and a strong advocate of the 60/40 portfolio, recommended a streamlined approach utilizing just two passive funds. He suggested investing in a US equity fund (advising against international equities as he believed the efficiency and potential returns were inferior) and an intermediate bond fund with a maturity period ranging from 5 to 7 years. This simplified execution made the 60/40 portfolio accessible to a wide range of individual investors focusing on long-term goals rather than navigating complex investment decisions.

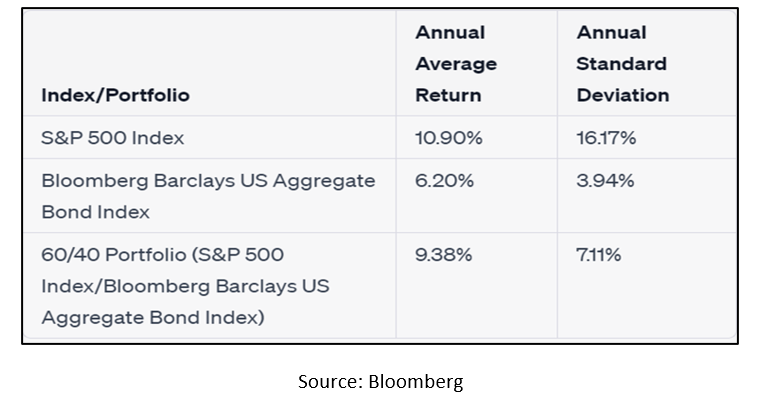

In addition, and almost irrespective of the above, a compelling attraction of the 60/40 has been its excellent and consistent performance for decades. Over the 50 years from 1971 to 2021, utilizing the S&P 500 as the equity component and the Bloomberg Barclays US Aggregate Bond Index as the bond component, this portfolio has returned an annual average return of 9.38 percent. In comparison, the equity benchmark returned barely 20 percent more, or 10.90 percent, but with double the volatility (see Table below)! The real bonus behind this outstanding performance was the bond component turning out to be a crucial source of return in addition to being a diversifier considering its very low correlation with equity (~ 0.15) … this, until the wake-up call of 2022!

Was the 60/40 success all about a big bond rally? Yes …

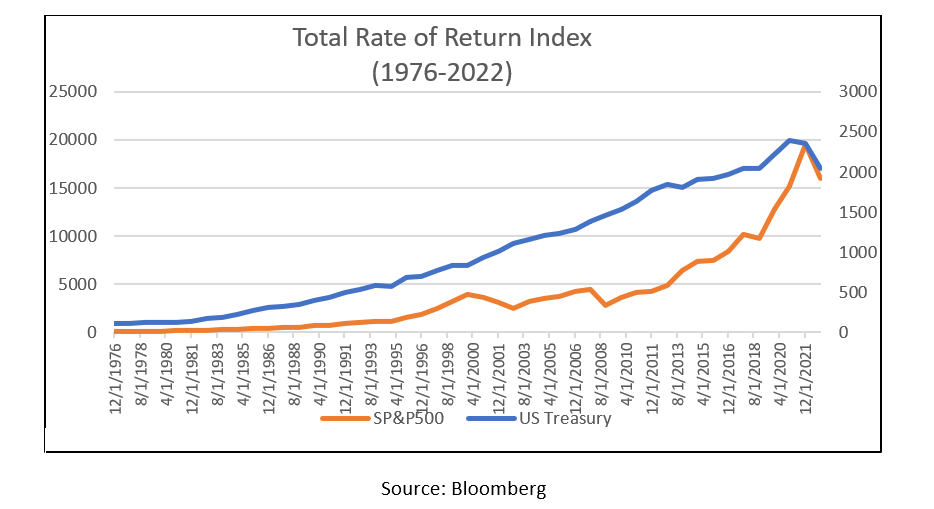

In the first quarter of 2022, a sudden surge in inflation and aggressive monetary policy tightening led to sharp declines in both bond and equity markets. Surprisingly, the losses in equities and bonds were nearly equal, with both asset classes experiencing a decline of around 16 percent. By the end of the year, equities and bonds had lost 18.13 percent and 13.01 percent, respectively. Initially dismissed as short-term fluctuations, the surprising losses have caused many to question the validity of the 60/40 approach, particularly considering the substantial losses in bonds. Indeed, the resulting raging debate highlighted an inconvenient truth: the attractive performance of the 60/40 portfolio was in large part attributable to the historical and uninterrupted massive bond market rally (see Graph below), an event hardly unlikely to be repeated!

While it is rational to expect the correlation between bonds and equities to eventually revert to its historically low norm, there are equally rational and thorough arguments predicting a continued rise in real yields back to their “natural” level (… and a decline in bond prices). Consequently, the 60/40 portfolio can no longer be relied upon as a winning, passive-like strategy justified by its historical returns. Rational analysis suggests that the landscape has shifted[1], necessitating a sharper assessment of the 60/40 potential performance going forward.

Back to the real Markowitz? Yes, finally …

The resulting and ongoing debate surrounding the validity of the 60/40 portfolio has sparked renewed interest in efficient and optimal portfolio construction, aligning with the principles laid out by Markowitz. The discussion has emphasized the importance of utilizing a proper optimization process to determine the optimal asset allocation rather than relying on a predetermined (preconceived!) 60/40 allocation as a one-size-fits-all, cookie-cutter approach and its subjective variations.

In essence, the discussion highlights the need to move beyond a simplified approach and embrace more sophisticated methods to achieve optimal portfolio construction, considering individual investment objectives and a broader range of asset allocation and investment selection possibilities. I.e., it highlights the benefits of considering a much more extensive universe of uncorrelated opportunities to not only diversify risk but also increase return potentials.

Indeed, Markowitz’s groundbreaking work in 1952 coincided with a time when the investment landscape was relatively limited, offering few choices to investors. It took several decades for various investment options to emerge and gain recognition. For instance, the first index fund was introduced in 1976 by John Bogle and Vanguard. Real Estate Investment Trusts (REITs) were established by the US Congress in 1960. The advent of junk bonds occurred in 1977 (note, more correlated with equities than with bonds). The launch of the first S&P 500 Exchange-Traded Fund (ETF) took place in 1993, coinciding with the acceptance of Emerging Market bonds as an investment option. Private equities became more accessible for trading in the late 1990s. The concept of factor investing gained traction in the 1990s and 2000s, following the influential work of Eugene Fama and Kenneth French. I.e., with so many not perfectly correlated alternatives, Markowitz’s work and diversification tenet would be even easier to prove!

These developments expanded the range of investment alternatives, each offering distinct returns, variances, and correlation structures. Investors now have a diverse and abundant universe from which to construct efficient and customized portfolios that aim to achieve higher returns for a given level of risk, or lower risk for a given level of return. The availability of these investment alternatives has significantly enriched the investment landscape and provided opportunities for more sophisticated and, crucially, customized portfolio construction strategies closely matching investors’ goals and risk preferences.

Indeed, with today’s avalanche of free data, computing power, AI, InvestTech, low-cost ETFs, and financial innovation, there is tremendous scope to build highly diversified and customized portfolios closely matching the investor’s risk tolerance profile and goals … a quantum leap from the cookie-cutter 60/40 dull strategy and its arbitrary variations. There are now ~11,000 (and counting) ETFs providing cheap and effective exposure to countries, markets, asset classes, factors (e.g., growth, value, low volatility, etc.), sectors, industries, and themes (e.g., ESG), forming an extensive treasure trove for the modern wealth manager willing and able to truly espouse Modern Portfolio Theory. The menu for the free lunch is now extensive, varied, and Michelin-starred!

Accordingly, and even if the optimal allocation turns out to be 60/40, what ought to be more relevant is what goes into each bond and equity bucket. Limiting the composition to two or three highly aggregated benchmarks completely ignores the power of diversification and optimization as it assumes that all securities within the benchmark have the same return, volatility, and correlation structure. Such a narrow approach fails to fully harness the benefits of portfolio construction and completely snubs the famous Free Lunch of portfolio construction at the expense of the investor.

Is there only one Efficiency Frontier? Yes … one for each separate set of investment alternatives.

One more powerful evolution of MPT: rather than relying on the arbitrary 60/40 and its highly subjective conservative, moderate, and aggressive variations derived in turn from a purely theoretical, single, all-encompassing Efficient Frontier, investors can benefit from a more tailored (and practical) approach to portfolio construction by first selecting their investment universe, and then apply MPT to build a bespoke Efficient Frontier[2]. The key concept is to prioritize the alignment between the investment universe and the investor’s objectives by selecting a set of investments suitable to individual risk preferences and objectives. For instance, a conservative investor seeking capital preservation would find little value in including highly volatile assets like Bitcoin or private equities in their portfolio. Conversely, an aggressive investor with a focus on capital growth would not benefit from allocating resources to utilities or intermediate treasuries.

By adopting this approach, investors can build portfolios that are better suited to their individual circumstances, allowing for more effective risk management and the pursuit of their specific investment objectives. Customization ensures that portfolio composition reflects the investor’s risk profile and goals, resulting in a more targeted, optimized, and successful investment strategy. Note that this is very much in line with Markowitz’s teachings who never postulated that MPT should be applied to a (theoretical) single universal set of investments out of which build an all-encompassing single Frontier. He simply optimized the set of investment alternatives he selected to prove diversification!

In conclusion, the 60/40 may be dead … but MPT is alive and well.

While the 60/40 approach may rapidly become obsolete, the debate over its value (and death) has bolstered the teaching of MPT and stressed the benefit of extensive diversification as the most efficient portfolio construction methodology. No question that proper asset allocation presents challenges compared to the old wealth advisory one-size-fits-all 60/40 approach. However, with today’s avalanche of free, real-time data, computing power, AI, modern investment digital platforms, availability of low-cost ETFs and zero-commission brokers, etc. the task of building customized portfolios that closely match the investor’s risk profile and goals is not just eased but is rapidly becoming the norm.

This shift represents a quantum leap from the old cookie-cutter solution, as investors now have the tools and resources to construct portfolios that are tailored to their specific needs. As technology continues to evolve, customization in portfolio construction, i.e., selecting the set of investment alternatives first and then optimizing, is rapidly becoming the new norm in the wealth management industry.

San Francisco – Spring 2023

[1] For example, and assuming that the recent bout of inflation may be temporary, there is the nagging issue of Quantitative Tightening, or the Central Banks’ aspiration to shrink their balance sheet back to “canonical” levels, which will continue to put downward pressure on bond prices for the foreseeable future.

[2] Following this approach, LGI has devised a set of Predefined investment universes classified by risk tolerance (conservative, moderate, aggressive), objective (Income, capital preservation, capital accumulation), and style (factor-tilted, global passive), each then generating specific Efficient Frontiers. Visit www.lumenglobalinv.com.